How does it increase your pricing?

It simply increases your ‘risk’ to not being paid. (NOTHING is truly FREE).

And why do you need a useless gimmick aimed at those that can’t truly afford to buy the home, thus increasing that ‘risk’ again?!

Just raise your fees straight out. It sounds like you cater to too many of the types mentioned above!

2 Likes

FHA, VA and USDA all allow for the cost of an inspection to be financed into the loan so it shows on the HUD 1 statement as an “Inspection Fee”, it is not uncommon.

2 Likes

I think he means it allows for folks to sell more ancillary services, which some use to raise that overall inspection fee. PAC has proven to do this for folks that are now using it. The client does not need to come up with the extra cash to pay for things like radon testing, mold testing, sewer scans, pool inspections, termite, etc… They just add those extra services on and do the PAC.

The reality is that a pay at close option really is not that different than offering a CC payment and putting the transaction fee on the client. If they choose to use the services they have to pay.

To top it off most people are under contract before they use our services, whether they can afford the home or not. And as far as pricing, its all about perceived value. You could be the most experienced inspector with the best reports, but the client isn’t going to care until they hire you. I could charge $200 more than the other guy but if I have more “bells and whistles” than the other guy, it increases my closing ratio.

By doing this, We will have either an incentive to see that the Home sells/closes or we give that perception. It is a clear conflict in my opinion. Over the past almost 13 years I have been asked maybe a dozen times if this is when my client is to pay me. After I tell them the reason I do not do that as I do not and should not have any incentive in seeing that the sale goes through…They respect that stance.

This is the reason there is really No Such Thing as a “Buyer’s Agent”…They only get paid if the home sells (in most cases)…They are in clear conflict (IMO) when representing their client…Buyers agents have a fiduciary obligation to (with) the Seller (not their client). We should not migrate into that same Conflict of Interest/muddy swamp.

5 Likes

I could see the perception from the general public, but if we get paid upfront and the bank gets paid regardless whether they close or not, I don’t see the validity. We are also underpaid, every little excuse I can find to charge more, I try to do. Within in reason of course ![]()

I’ve looked heavily at the Guardian Pay At Close program and sat through a webinar.

The main reason I have NOT signed up is the hefty $75 fee that you are not allowed to pass along to the consumer.

Guardian and their fans say, yes, but you’ll sell more ancillary inspections, and your avg ticket price will go up $250!

But profit margins on inspections are roughly 20% by the time you pay for over head, employee salaries, employment taxes, tools, healthcare, workman’s comp and other expenses.

20% of $250 is $50. Subtract $75, and now we’re looking at ($50 profit - $75 fee) a potential $25 loss.

So I’m not seeing the benefit of taking on Guardian’s $75 fee to offer pay at close to watch profit margins go down.

Everyone who loves the Guardian program only talks about their gross going up, but no one wants to talk about if their profits go up.

6 Likes

This is on the same lines as most inspectors that set their fees based on what other inspectors fees are, without having any clue what their actual costs of doing business are!!

2 Likes

Yep… finally - here is a glimpse of what this actually “costs”. 1 in 20 doesn’t close AND refuse to pay so the company managing it has collected 75X20 (from us as HIs keep in mind) for 1500 and eats 500. This whole thing is starting to sound like the sleazy aftermarket car warranty companies that keep calling me!

5 Likes

That’s correct, Scott…as I recall it, too. ![]()

Nick, I’ve been looking at Guardian Financial’s spiel on this. I also started surveying new clients if having a pay-at-close option would be helpful and maybe 30% - 50% of the said it would Many homebuyers have little margin (i.e. not enough free cash) and are barely hitting the minimums required for out-of-pocket expenses.

While I personally do not advise financing this kind of thing, the reality is that they are already amortizing certain fees, the largest being the real estate agent’s commission.

Legally, one cannot charge extra for a pay-at-close option without further licenses and overhead (as this makes one a ‘lender’). So, to make a pay-at-close option worthwhile you would need to increase your fee structure in all cases. In reality, I suspect most inspectors offering a pay-at-close option use some sort of loophole, such as offering a discount for paying with credit card. However, If I could raise my rates across the board $125 I would have already done so. There are probably games that could be played to skirt these rules and still stay legal. I haven’t researched that fully yet.

The entire purpose of offering a pay-at-close option is to facilitate increasing the total inspection fee (inspection plus ancillaries) for clients exercising this option. Fully 50% of the calls I receive start with the words “I’m looking for a quote”. These calls typically do not translate into sales, as the caller is shopping for a cut-rate inspector and isn’t as concerned with quality, despite my best efforts to convince them otherwise. Some (or many) of these bargain-hunters are cash-poor and a pay-at-close option could be a potential game changer.

One other thing to consider is that pay-at-close includes paying for closing costs out of pocket as well as rolling the closing costs into the loan. The latter is particularly attractive to many people, although I personally wouldn’t advise it.

So, yes, I think a pay-at-close infrastructure would be a very beneficial service to have available, especially to help convert bargain-hunters and the cash-poor into clients.

BTW, a great deal of the risk (house not making to closing) can be avoided by getting a credit card from the buyer, performing a test charge ($0.01) and then charging the card if the deal doesn’t make it to closing. This appears to be Guardian’s procedure. It’s not much riskier than what most of us do already with credit card payments. Interestingly, I’ve never had a client try to reverse charges or close their credit card if they decided not to purchase the home.

5 Likes

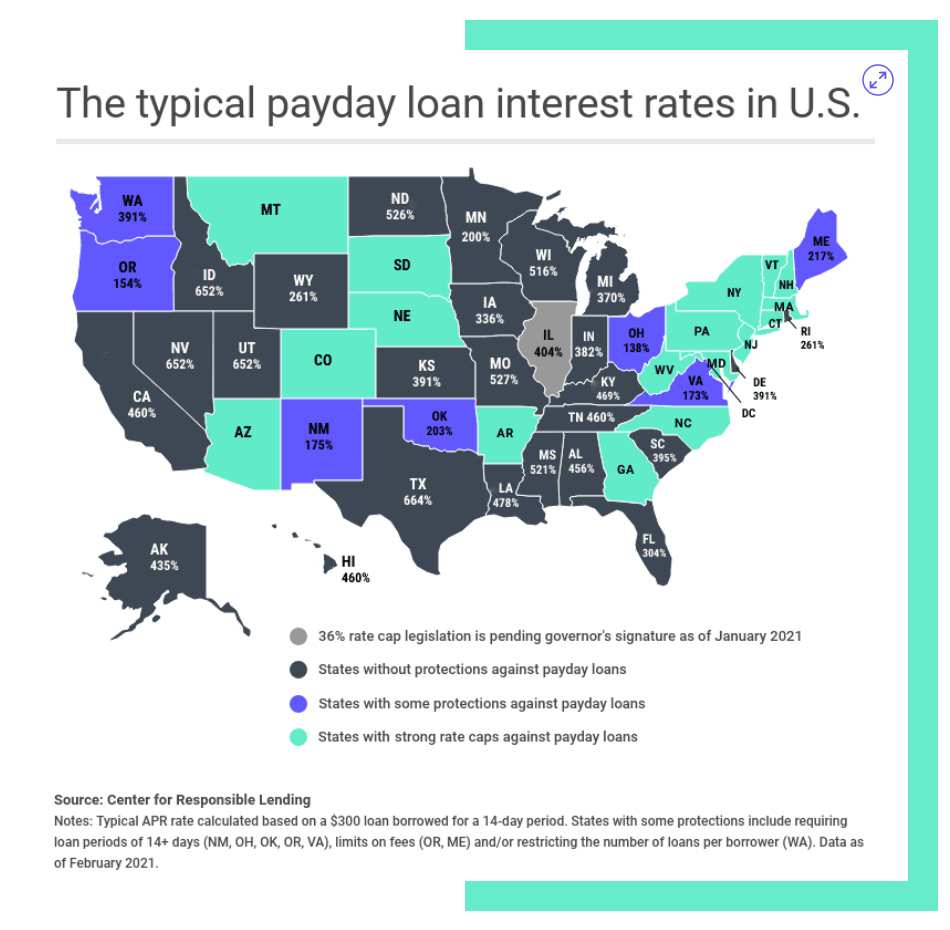

I’m pretty sure none of my customers would be stupid or desperate enough to pay $150 to defer a $800 inspection fee for 14 days. That’s 450% annual interest, which is more than the average payday lender charges.

6 Likes

So most of those at retail are “interest free” if you pay on time. It’s the retailer paying the bill, much like they pay a % to accept credit cards. It’s a way to get consumers to spend more. The business model seems to be the pay on time customers are loss leaders for the real business of soaking those that pay late:

Don’t expect similar legislation in the USA.

2 Likes

I read that entire article and it did a poor job of illustrating how the consumer was harmed. The government over taxes its people so they go into debt. It’s true in almost all heavily taxed countries. Funny how the government acts as if it is a consumer advocate.

3 Likes

This is a freedom of choice issue as well. It’s clear that things like smoking, problem gambling and debt spirals happen: and predatory companies will profit. What’s the government role? Prevent that? Make sure disclosures are clear? Add such consumer issues to curriculum in primary school?

Either way “buy now pay later” is getting big and perhaps profitable

I saw a Logo of the Pay for Your Inspection at Closing on the forum. Does this mean the program is being rolled out?

1 Like

I would be interested.

Here is another company who offers this service for $75. But of course, you have to use their cc processing.

Not sure which is worse. The scammers that will only communicate via text or email or the phone calls and emails from actual companies or INACHI venders that are peddling their services.

2 Likes